UK independent schools are world renowned for their excellent quality of education and student prospects. Indeed, the 2020 Independent Schools Council annual consensus showed that of the 537,315 students attending independent schools 90% went onto higher education. The majority, 51%, went to one of the top 25 UK universities of which 5% chose to study at Oxbridge. It is not the education alone that sets these schools apart. They often have exceptional facilities, offer a myriad of extracurricular activities, and have a diverse cohort of international students, all of which cultivates the mind and character of students.

Worth the Cost?

However, such a start to a child’s life comes at a substantial cost. Whereas a state school will on average cost the taxpayer around £6,000 per year, independent schools can charge anything from around £13,000 a year up to £40,000 at a top boarding school. Over five years, this represents a considerable financial commitment and hopefully one that will yield enormous returns in a child’s later life.

To be able to provide for this education can for many seem like an unachievable aspiration. However, with a few simple steps one can come closer to realising this ambition through investment.

A segregated investment pot offers some peace of mind that this commitment could be met regardless of job security and increases in schooling costs (which have risen faster than inflation since 2000). Furthermore, if a family is willing and able to assist, they may consider asking for the gift early on. If received and invested now, as explained in Step 3, the sum can produce returns that pay for the school and means the donor does not have to part with as much to begin with.

*Please note that the following principles can also be applied to meet other goals for one’s children. These may be ensuring the children begin their adult lives without the cost of student debt by paying for university, or perhaps even providing the deposit on their first property.

1. Plan ahead

The first step on this journey is deciding whether to send children to an independent school and take on the necessary financial commitment. The earlier this decision can be made the better as one can begin to set aside surplus cash from, for example, salaries, bonuses, gifts or inheritances in order to invest it specifically for schooling.

2. Choose an investment ‘wrapper’

Next it is important to take advantage of the many ways in which investments can be held. Think of the investment wrapper as the basket that holds the investments, different baskets have different purposes and advantages.

A common example of which is an Investment Wrapper. Some wrappers, insulate the investments from income tax and capital gains tax. Therefore, it is well worth exploring the different tax-efficient options available to maximise saving potential.

3. Begin investing and stay invested

The importance of investing early is due to the simple but powerful force known as ‘compounding’. This is the idea of earning a return not only on the original investment but also on the accumulated interest that is reinvested. This may sound obvious or trivial, but the long-term effects can be startling:

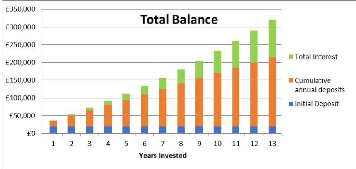

Take for example, if when a child was born the parents invested £20,000 into a stocks and shares ISA (the maximum allowance for tax year 2020/21), made annual contributions of £15,000 in monthly instalments, and invested in the market returning an annualised 5.3% per year. By the time this child went to school aged 13 – the investment would have grown to £320,831.70 (before associated costs). This would be enough to pay for two children to attend simultaneously (with today’s purchasing power).

This annualized return of 5.3% mentioned above represents the annualized total return investors have received over 20 years. This return is above the general rate of inflation, meaning investors have increased their ‘real’ wealth over this time. recognizing their most recent achievements. You can even invite more sociable aspects into the playing field by including pieces of fluff information, such as newlyweds and parents-to-be within the office.

It is important to emphasise that markets fluctuate in the short term due to many factors including global crises and periods of rapid economic growth. Generally speaking, over the long-term markets trend upwards. This is because investors are rewarded for tolerating the extra volatility (risk) of the stock market. This is why the annualised growth remains positive even during the recent period that saw the Coronavirus sell-off, the Global Financial Crisis and the bursting of the Dotcom Bubble.

The old investment adage remains true: “It’s about the time in the market rather than timing the market.” Therefore, to reiterate, begin investing and stay invested.

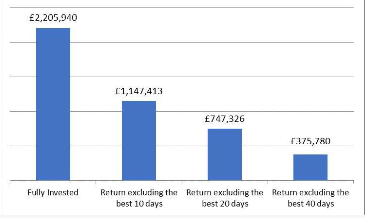

To withdraw funds during tumultuous times is a temptation many investors succumb to. However, the best days of market returns tend to follow shortly after the worst. Indeed, being fully invested (not withdrawing funds and reinvesting dividends) in the FTSE All Share for 20 years would have given an investor almost double the money compared to someone who missed the best 10 days in the market. The results are even bleaker if an investor missed the best 20, let alone 40, market days as money would have been lost. The below chart illustrates how much a portfolio would be worth this year with a £1million investment made in 2000:

4. Consider additional costs on top of the school fees.

The full benefit of independent schooling derives from the extracurricular activities offered such as school trips and music lessons. Though formative for the students, these can place an additional financial burden. It is important to plan ahead for these eventualities and factor additional costs into financial planning.

5. Commit to being able to pay for the duration of their school life.

Leaving a school can be difficult for both the child and family. Unfortunately, being unable to continue paying the fees can happen. Whilst we can never be sure what the future holds, it is important to protect a child’s education. One way of achieving this is by reducing the investment’s exposure to risk in the run up to, and during, children’s schooling. As discussed in Step 3, investors are typically rewarded for taking on higher market volatility with higher market returns. However, moving a portfolio into traditionally less volatile assets (such as fixed interest and cash), provides ballast against market downturns and gives greater certainty that fees can be met.

Final Thought

Whilst the above steps, I hope have helped demonstrate how one may be able to pay for an independent schooling, or any other financial goal for a child’s future, professional help is available at every stage along the way. A Financial Advisor can help finesse a tailor-made solution to evolving circumstances and objectives. Moreover, a dedicated investment manager would devise and manage an appropriate portfolio of assets to meet individual goals. Such services do add additional costs to the investment process but provide expertise and access to assets only available to investment institutions. We in the financial services aim to simplify and enhance the investment experience.